Group of Fools

(Any views expressed in the below are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.)

The dollar-yen exchange rate is the most important macroeconomic indicator. In my last essay, “The Easy Button,” I wrote that something must be done to strengthen the yen. The solution I proposed was that the US Federal Reserve (Fed) could swap unlimited amounts of freshly printed dollars with the Bank of Japan (BOJ) for yen. This would allow the BOJ to give unlimited dollar firepower to the Japanese Ministry of Finance (MOF), with which they could purchase the yen in the global forex markets.

While I still believe in the validity of that solution, it appears that the central banking charlatans in charge of the Group of Fools, a.k.a. the Group of Seven (G7), have chosen to convince the market that the interest rate differential between the yen and the dollar, euro, pound, and maple syrup (Canadian) dollar will narrow over time. If the market believes in this future state, it will buy yen and sell everything else. Mission accomplished!

For this magic trick to work, the G7 central banks (the Fed, European Central Bank “ECB,” Bank of Canada “BOC,” and Bank of England “BOE”) with “high” policy interest rates must cut them.

The critical thing to note is that the BOJ’s policy rate (green) is 0.1%, whereas everyone else is 4–5%. The interest rate differential between the home and foreign currency fundamentally drives exchange rates. From March 2020 until early 2022, errbody played the same game. Free money for all as long as you stay inside with the flu and shoot up that mRNA heroin. When inflation showed in such a big way that the elites could not ignore the pain and suffering of their plebes, the G7 central banks — with the exception of the BOJ — all raised rates aggressively.

The BOJ could not raise rates because it owns over 50% of the Japanese Government Bond (JGB) market. JGB prices pumped as rates dumped, making the BOJ appear solvent. However, the highly levered central bank would suffer catastrophic losses if the JGBs it held declined because the BOJ allowed rates to rise. I did some scary maths for readers in “The Easy Button.”

This is why if the decision by Bad Gurl Yellen, who calls the shots at the G7, is to reduce the interest rate differential, the only option is for the central banks with “high” policy rates to reduce them. In orthodox central bank thought, cutting rates is good if inflation is below target. What’s the target?

For some reason, and I don’t know why, the inflation target for every G7 central bank is 2%, irrespective of differences in culture, growth, debt, demographics, etc. Is the current inflation rate hurtling through 2%?

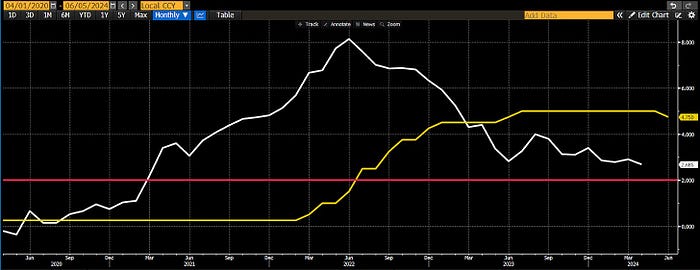

Each coloured line represents a different G7 central bank’s inflation target. The horizontal line is at 2%. No G7 country’s manipulated and dishonest government-published inflation statistic is below target. Putting on my technical analysis hat, it appears that G7 inflation is forming a local bottom in the 2–3% range before exploding higher.

Taking that chart into consideration, an orthodox central banker would not cut rates at their current levels. However, this week, the BOC and ECB cut rates while inflation was above target. This is strange. Is there some financial disturbance that demands cheaper money? Nope.

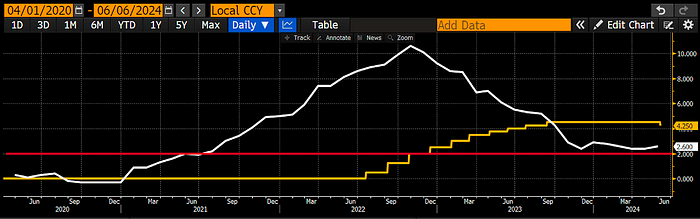

The BOC cut its policy rate (yellow) while inflation (white) is above the target (red).

The ECB cut its policy rate (yellow) while inflation (white) is above the target (red).

The problem is the weak yen. I believe Bad Gurl Yellen stopped the rate hike Kabuki theatre performance. It is time to get down to the business of preserving the Pax Americana-led global financial system. If the yen isn’t strengthened, the big bad pinko commie Chinamen will unleash the dragon of a devalued yuan to match their chief export competitor Japan’s super-duper cheap yen. In the process, US Treasuries will get sold, and that will be game, set, and match for Pax Americana if it occurs.

Next Up

The G7 meets in a week. The communique released after the meeting will greatly interest the market. Will they announce some sort of coordinated currency or bond market manipulation exercise to strengthen the yen? Or will they stay quiet but agree that everyone except the BOJ should begin cutting rates? Stay tuned!

The big question is whether the Fed will start cutting rates this close to the November US presidential election. Typically, the Fed doesn’t change course this close to an election. However, typically, the favoured presidential candidate is not staring down a potential prison sentence, so I’m ready to be flexible in my thinking.

If the Fed were to cut at its upcoming June meeting whilst their favoured doctored measure of inflation was above target, the dollar-yen would gap lower bigly, which means the yen would strengthen. I don’t believe the Fed is ready to cut rates, given that Slow Joe Biden is getting skewered in the polls over rising prices. American plebes understandably care more that the vegetables they eat are more expensive than the cognitive ability of the vegetable running for reelection. To be fair, Trump is also a vegetable because he loves munching McDonald’s fries and watching Shark Week while doin’ his thang. I still think it’s political suicide to cut rates. My base case is the Fed holds.

By the time the dilettantes sit down for a sumptuous meal paid for by their tax-paying subjects on June 13th, the Fed and BOJ will have conducted their June policy meetings. As I said before, I expect no changes to monetary policy from the Fed or the BOJ. The BOE meets shortly after the G7, and while the consensus is they hold their policy rate steady, I think we are in for a surprise to the downside, given the BOC and ECB cuts. The BOE has nothing to lose. The conservative party is going to get their ass handed to them at the next election, so there is no reason to disobey orders from the rulers of their former colony in order to keep a lid on inflation.

Exit the Choppa Zone

The June central banking fireworks kicked off this week by the BOC and ECB rate cuts will catapult crypto out of the northern hemispheric summer doldrums. This was not my expected base case. I thought the fireworks would start in August, right around when the Fed hosts its Jackson Hole symposium. That is typically the venue where abrupt policy changes are announced going into autumn.

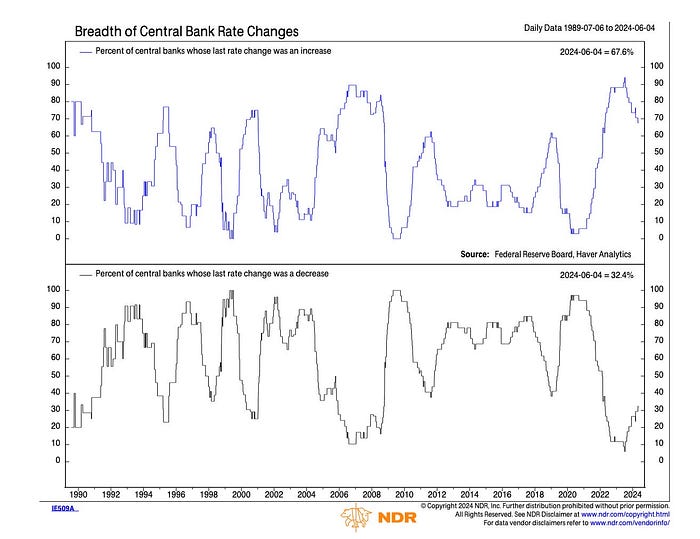

The trend is clear. Central banks at the margin are starting easing cycles.

We know how to play this game. It’s the same fucking game we have been playing since 2009 when our Lord and Saviour Satoshi gave us the weapon to defeat the TradFi devil.

Go long Bitcoin and subsequently shitcoins.

The macro landscape has changed vs. my baseline. Therefore, my strategy shall change as well. For the Maelstrom portfolio projects, who asked for my opinion on whether to launch their tokens now or later. I say, Let’s Fucking Go!

For my excess liquid crypto synthetic-dollar cash, a.k.a. Ethena’s USD (USDe) that’s earning some phat APYs, it is time to deploy it again on conviction shitcoins. Of course, I’ll tell readers what those are after I have purchased them. But suffice it to say, the crypto bull is reawakening and is about to gore the hides of profligate central bankers.