Thanks for Nothing

(Any views expressed in the below are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.)

n August of 2006, I stepped off of a Cathay Pacific flight into my future home of Hong Kong for the first time. Welcome to study abroad! The previous semester, I applied and was accepted into the Hong Kong University of Technology’s program.

Two years prior, before I began the 21st century rite of social passage called university, where one spends 4 years learning how to hold one’s liquor and other things like CAPM, I decided to chase growth. That meant Choyna. I enrolled in the Chinese language program. After two years of Chinese classes five days a week, I was OK at speaking, could hold a conversation, and write almost a thousand characters — but I was in no way, shape or form anywhere close to fluent.

Without a full mastery of Chinese, I could not enroll in the Fudan program in Shanghai, as fluency in Mandarin was required. So I chose the next best thing after real China — Hong Kong.

My first memory of Hong Kong is always with me, and evokes a strong sense of nostalgia. Like a complete noob, I disembarked, collected my luggage, and — brandishing a piece of paper with my university’s address — got into an unmarked car (because some dude hustled me in the arrivals hall). As I became a more seasoned traveler, I quickly learned to never ever get into a non-licensed taxi.

If you haven’t taken the drive from Hong Kong airport across the New Territories into Sai Kung at night, it is one of the most magical drives in the world. Driving across the Tsing Yi bridge, you witness the most impressive skyline in the world, anchored by a fragrant harbour buttressed by skyscrapers in Kowloon and Hong Kong Island. As you cross into the Sai Kung Country Park, down the mountainside, the pitch-black sky is dotted with the lights of country houses and fishing vessels.

After about 45 minutes in a van (… down by the river) I arrived on campus. It was late at night, but I still managed to register and got the keys to my dorm room. I hadn’t taken two steps into our room before my roommate — who I had never met in my life — ordered me to “put [my] shit down,” because we were “going to Lan Kwai Fong”. He seemed to know what he was doing, so I complied, and I went bar hopping for my first (but certainly not last) time in LKF.

Availing myself of the region’s trains and planes, I witnessed the breakneck growth of China post-WTO inclusion through my visits to Shenzhen and Beijing that semester. Oh, how the cities have changed over the subsequent 15 years.

There was no doubt in my mind after I returned to Philadelphia that I would live in Hong Kong. My next goal was to secure a summer internship. I already had an offer to return to JP Morgan in their investment banking program that summer, but they denied my request to transfer my offer to their Hong Kong office. I then applied online to every single major investment bank’s Hong Kong internship program.

Luckily, I secured an on-campus interview with Deutsche Bank, and converted that into a summer job. I have already regaled regular readers of my newsletter with vignettes of my 12 weeks spent between Hong Kong and Singapore, so I’ll fast forward a bit to get to the point of my story.

The time period was 2009 to 2013. The 2008 Global Financial Crisis severely impacted all countries, but without the Chinese industrial expansion — funded by the largest increase in sovereign debt in human history — the GFC’s negative impact would have been much greater. China built cities for hundreds of millions of its citizens in under a decade. It became far and away the biggest buyer of essential commodities in the world. Its burgeoning class of uber-wealthy comrades fanned out across the globe and spent billions enjoying the finer things in every major tourist destination. In short, the China growth story completely altered the global economy in many ways.

Mutual fund indexing and the invention of the exchange traded fund (ETF) is one of the biggest contributors to greater market access in financial markets history. The ETF allows all types of investors to access different asset classes that, on their own, are extremely expensive or downright impossible to invest in directly. As with most emerging markets, high growth comes with various capital market restrictions on foreigners. China during this time period was no different. The ETF structure became the gateway for foreign capital into the Chinese equities market.

As the world watched the voracious Chinese rapidly urbanise and industrialise, non-Chinese investors wanted a piece of the companies participating in this debt-fueled growth “miracle”. Beaucoup profits were to be had by trading China A-share companies listed in Shanghai and Shenzhen. However, with a closed capital account, Chinese equity markets sat just out of bounds.

In order to allow some foreign investment, a scheme called the Qualified Foreign Institutional Investor program (or “QFII”) was created. Each large, global investment bank received a fixed QFII quota administered by Chinese regulators. With this QFII quota, banks were free to buy and sell China A-share stocks.

One of the most profitable activities for the Hong Kong branches of bulge bracket investment banks was giving clients access to China through the QFII program. Traditionally, this was done using an Equity Total Return Swap, but iShares (2823 HK) and BOCI Prudential (2827 HK) took steps to make the process easier by creating an ETF vehicle listed in Hong Kong that would give investors access to China A-shares. To do this, the fund manager bought China A-share TRS from investment banks with QFII. The banks charged ginormous swap fees, because they had access and no-one else did. So pay the toll, bitch.

DB teamed up with BOCI and was the sole swap provider and designated market maker for 2827. That meant a glorious stream of economic rent for DB as the bank doled out access to the China market to its clients.

As the grad who was hired to take over the ETF business, my destiny was managing the 2827 book. After a period of 6 months, my boss felt I wasn’t fucking up too much and handed over the reins to me. To say I was scared shitless is an understatement. Using the QFII allocated to 2827, my job was to maximise economic rent. I controlled creations, redemptions, and set the premium or discount at which the ETF traded in the open market each day. While I was there, 2827 / China was the only profitable segment of DB’s ETF business.

Over time, DB launched other swap-based ETFs offering access to the Chinese market. One notable standout was 3049 HK, which tracked the CSI300. It was our answer to the behemoth that was the iShares 2823 FTSE A50 ETF. Over time, I gained control of a significant chunk of DB’s QFII allocation, which meant almost guaranteed profits for our desk and a phat bonus for my big boss. Please note, shit rolls downhill, but the bonus pool stays at higher altitudes than a junior trader.

The first iteration of China-access ETFs featured foreign banks with a fixed allocation of dry powder to deploy in China. They all charged hefty fees to the world that wanted access to the hottest economy in the world, China.

As with all golden geese, they got slaughtered. The Chinese asset management companies (AMC) did not sit idly by and watch a bunch of south-bound locusts consume all the fat from the market. The major mainland asset managers set up Hong Kong subsidiaries that received a separate allocation of CNH (or offshore Renminbi) and approval to hold physical Chinese equities, named RMB Qualified Foreign Institutional Investor (RQFII).

Each of the large China AMCs received a large equity index to replicate via a Hong Kong-listed ETF. Each AMC received a RQFII quota. This quota was superior to QFII because fund managers offered physically-backed ETFs, which meant they sidestepped the hefty swap fees charged by the foreign investment banks.

These ETFs launched in the summer of 2012. Even though the AMCs had the juice, they still needed the market making expertise of the large foreign banks. Therefore, as the head ETF trader at Citibank, I had to make markets in Hong Kong on the RQFII ETFs, and as a perk I could create and redeem these ETFs at their Net Asset Value (NAV).

The market initially did not appreciate how valuable the RQFII quota would become. I convinced my bosses to let me take down a massive amount of RQFII exposure, and hedge it with short futures contracts. I went long the ETF at NAV, and hedged progressively by shorting futures contracts at a premium. Cash and carry 101, brah.

I then doled out the goodies to valuable clients at the firm, because I’m a franchise guy. You want some RQFII, 100bps please. Pro-tip, a franchise guy is a trader that loses money, gets paid less, but their sales counterpart racks up “sales credits” that have nothing to do with the overall profitability of the trade — guaranteeing that the salesperson is client-friendly and enabling them to get a bigger bonus. I might be a little salty … just a little … all those flavours … still salty.

In 2013, I received a pink slip, found the one true god Satoshi, and the rest is history. Now, let’s take the lessons learnt from my China experience and apply them to the launch of the bitcoin futures ETFs in the US last week.

When there is an asset or market that has past and present amazeballs returns, but for a variety of technical and regulatory reasons cannot be accessed by the vast majority of retail and institutional investors, there is an opportunity to create an access product in the form of an ETF that generates economic rent for the fund manager. Bonus points if the instruments purchased to generate exposure to the asset are derivatives. With derivatives, there exists a greater ability to skim cream from insto investors frothing at the keyboard for dat alpha.

I hope this story about my journey through ETFs and China gives you the confidence that I know what I’m talking about as I walk through the intricacies of the recent ETF launches. Because the ProShares ETF’s AUM is approx. 240x bigger than the Valkyrie ETF, I will focus solely on the ProShares ETF.

Futures vs. Cash

For a variety of reasons that aren’t important to this essay, the SEC telegraphed quite clearly that a futures-based bitcoin ETF could receive approval. The most famous disapproval came in March 2017 on the back of the Winklevoss Bitcoin ETF, COIN.

I vividly remember that trading day. Budding shoots of a crypto bull market presented themselves as the price started the year by breaking $1,000. By March, the price hovered around $1,200. But the market focused on whether the SEC would finally allow the ETF to proceed. NYET SHITCOIN, they said. And the price of bitcoin dropped 30% in 5 minutes. Waaaah, such volatility, much investability.

Subsequent fund managers listened and presented applications based on the CME bitcoin futures. The ProShares Bitcoin Strategy Fund (BITO US) launched last Tuesday. In order to generate exposure to bitcoin, the fund purchases front-month futures contracts.

Each CME bitcoin futures contract is worth five bitcoin, and they have monthly and quarterly expiries. The most liquid contract is the next-calendar-month contract. The market is fairly liquid, but a variety of non-US domiciled platforms offer more liquid markets. A key point about these futures contracts is that they are margined in USD, and bitcoin cannot be used as margin collateral.

The main takeaway is that a futures-based ETF is more expensive for the end user than a physically-backed ETF, for a variety of reasons.

- Futures trade at a premium or discount relative to the cash or spot value. In bitcoin, the futures usually trade in contango because bitcoin can pump to infinity, but can only dump to zero. Also, very important — unlike a commodity, the supply of bitcoin is fixed, irrespective of the price. For example, as the price of gold rises, certain deposits become economical to mine and supply increases, which dampens prices. Even if bitcoin instantly rose to trade at $100,000, there would only be so many bitcoin mined each block — which almost necessitates a futures curve in contango.

- The fund must roll futures contracts every month. The roll costs money, as the fund manager must cross a spread. That cost is passed on to holders of the ETF.

Fund Disclosures

There is no surfeit of data, given the ETF only began trading last week. But let’s walk through the types of information the fund provides us investors to assess its performance. Here is a link to the page where ProShares provides this information.

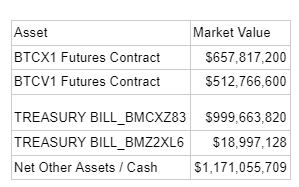

The first piece of data that is published every day are the fund holdings. As of 22 October 2021, the ETF held the following assets:

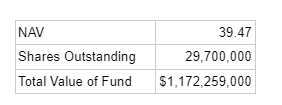

The next table describes the value of the fund based on shares outstanding and the NAV. The NAV is calculated as of 4pm Eastern Standard Time. Remember this timestamp — it is very important in order to understand the future market microstructure impact of this and other ETFs.

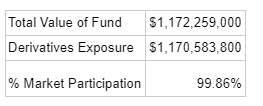

The first thing I want to know is, how invested is the fund in instruments that should track the price of bitcoin?

This is a good sign. The fund is buying enough futures contract notional to track the price of bitcoin.

One thing that stood out to me is the massive amount of cash held by the fund. The fund holds almost double the amount of cash vs. the notional value of the futures contracts. The CME does have quite restrictive margin requirements, but the initial margin is 50%, not 200%. My trusty research assistant delved deep into the prospectus and uncovered that the fund avoids capital gains taxes if the amount of cash is kept at these levels.

If I create $100 worth of ETFs, the fund needs to provide another $100 from its own pocket in order to receive this favourable tax treatment. That is massively capital inefficient. It serves as a large barrier to entry to any would-be fund advisor at scale. The one benefit of the excess cash is that it will be very tough for the fund to get margin called. When you trade a product from 9:30am to 4pm by purchasing a futures product that doesn’t trade on the weekend, and the underlying assets trades 24/7 and likes to pump and dump on the weekends, rekt on open is a real possibility.

The one thing you don’t know from these daily disclosures are trading costs. Those will not manifest themselves in the total expense ratio, but rather in the net execution price of the futures contracts –and you must closely monitor the tracking error to notice how much money is being lost due to execution.

Tracking Error

The one opaque aspect of this fund (and many others) is what the tracking benchmark is. Because investors view this product as a vehicle to obtain bitcoin price exposure, let’s evaluate the fund based on how well it tracks the CME CF Bitcoin Reference Rate (BRR). Oh yeah baby, give me that BRR …

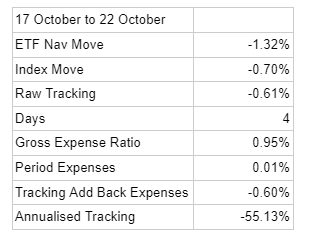

I calculated the tracking error from 18 October — 22 October. I compared the 4pm print of the BRR Index on the 17th vs. the 4pm print on the 22nd. I compared that with NAV returns from the 17th to 22nd. I then added back the fees paid to the fund [4/365 * 0.95%]. The below table is the result.

Yowzers! 55% annualised underperformance. Admittedly, this covers only 4 days of data. The magnitude might soften as time progresses — but still, it’s not off to a good start.

The roll cost is a major expense that must be paid every month if the futures curve is in contango. In this example, that means the nominal price of the November contract is higher than the October contract. The mechanics are as follows:

- You begin long October contracts, BTCV1.

- You execute a transaction whereby you sell BTCV1 and purchase BTCX1. This is called long rolling.

- Because BTCX1 Price > BTCV1 Price, there is a trading loss that holders of the fund absorb.

The fund will also pay commissions on every lot executed to its broker over and above the CME fees. Oh yeah baby, the banks love these derivatives-based ETFs — they guarantee massive commissions every single fucking month.

This is just something investors must accept, because there is no way around these execution costs. TINA is a cruel mistress.

Flo Rida

Now, while this product is suboptimal from a cost perspective to long holders, it is a great vehicle to channel fiat into the bitcoin markets. Channel your inner Cuba Gooding Jr. and “show me the money!”

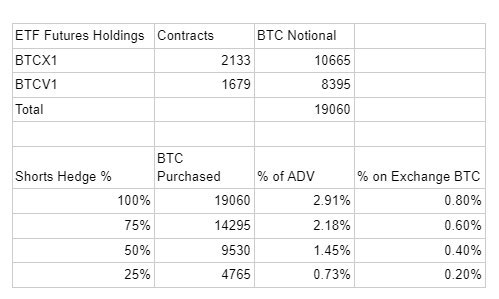

For every long, there is a short. That is axiomatic to any futures market. Therefore, the question is, do those who sell bitcoin futures contracts hedge their exposure by purchasing spot bitcoin?

The degree to which shorts delta hedge determines the amount of bitcoin purchased. At the margin, this should add upwards price pressure. Remember, the last trading price is determined by the marginal buyer. Long live flow over stock.

Imagine you are a CME participant hedging your short bitcoin exposure. You must purchase coin from an OTC dealer or an exchange. Even flow to OTC desks eventually ends up on the exchange. Therefore, the quantity of bitcoin available for purchase is that which is held on exchange. Glassnode provides a useful estimation of total exchange holdings.

At approx. 2.4 million BTC held by exchanges, the available supply for sale is 12.93% of all mined bitcoin to date. Not much lah!

Of those 2.4 million coins, only a fraction actually trade each day. The relevant figure is the average daily spot trading volume across the relevant exchanges. I constructed a handy chart which depicts what % of daily volumes the total AUM of the ProShares ETF represents. This gives us a yardstick to judge the marginal price impact of fund futures buying.

Based on the first 4 days of trading, it does not appear the flow of fiat generated much technical marginal price pressure. The upward move in bitcoin is based on the expectation that this and other funds’ AUM will grow massively.

The next forecasting question is, how large could the bitcoin ETF complex become?

There already exists a pseudo-ETF with over $40 billion in AUM, the Grayscale Bitcoin Trust (GBTC). It is not technically an ETF, but it hoovered up assets nonetheless. Therefore, what is required is not a movement of AUM from one tracker product to another, but fresh capital into the system.

When GBTC is added to the mix of US-listed tracker products, will there actually be net new demand from retail traders and institutions who aren’t already invested in the space? I fear that the narrative on institutional and retail investors plowing AUM into the complex might be misplaced, as those who want to be involved largely already are.

The one issue with GBTC is that creating units takes months, while BITO-created units settle in two trading days. Therefore, market makers on BITO can short sell BITO, create units, meet delivery, and collect any premium present in the market. That being said, long holders of BITO will get crushed by futures trading fees and the cost to roll positions each month. What is worse, a volatile premium on GBTC, but with no tracking error because it actually holds physical bitcoin, or a futures-based product with enormous tracking error, but no premium? Same same, but different.

It may transpire that the GBTC premium, which is known ex-ante, is cheaper than an ex-post, unknown tracking error of BITO. A bitcoin futures-based ETF is certainly a welcome development in the general adoption of bitcoin and crypto, but is by far one of the most expensive ways to acquire exposure compared with the alternatives already on the market. Will retail and institutional investors stomach the massive negative theta embedded in the plethora of US-listed, futures-based ETFs that will permeate the market?

Maybe I’m too harsh. Institutional investors are still dumb enough to purchase sovereign government bonds at zero-bound interest rates. When judged against global “transitory” inflation, most corporate and sovereign bond holders are mathematically guaranteed to lose money in real terms. Math, it seems, is a luxury of the few.

Tick Tock

If these US-listed ETFs continue to quickly grow AUM, the trading patterns of the spot bitcoin market will change. The majority of volume on any exchange with an opening and closing time, occurs at the open and close. The volume profile looks like a bathtub. US equity markets open at 9:30am EST and close at 4:00pm EST. Therefore, we can expect significant price discovery and volatility concentrated around those two times.

Another point of interest is the time at which the fund executes buy and sell orders to create and redeem ETF units. The process works as follows:

For a creation:

- An authorised participant (AP) submits an amount of USD cash to the fund to create a certain number of ETF units.

- The fund takes that cash, and then purchases futures contracts and transfers units to the AP.

- I am not sure how that execution is done. Sometimes the AP can specify to the fund how they would like the execution to happen. For example, if the AP wanted to match the close (4:00pm), the fund would pay a broker to match the 4:00pm futures print for a fee. Or, the fund could have complete discretion as to how the futures are purchased. It is unclear from the prospectus how executions will happen.

- One way to ascertain the method of execution is to find a day when the number of shares outstanding increased, and then review the CME executions for the front-month contract for any obvious abnormalities that would point to a specific type of execution.

For a redemption:

- An AP submits an amount of ETF units to the fund, to redeem and receive USD cash.

- The fund takes the ETF units and then long sells futures positions, which frees up margin. That cash is then transferred to the AP.

- Similar to creations, it is unclear how the sell orders will be executed.

As I mentioned before, the monthly roll of futures contracts will have a market impact. With its current holdings, the ETF represents over 20% of the CME bitcoin futures open interest (OI). Purely a guess, but the fund is the largest holder of contracts. Therefore, when they roll …. I get deep, I get deep, I get deeper!

A cash and carry futures arbitrage trader lives and dies by how they execute the roll. If you are a long roller as well, you want the basis or difference between the front and back contract to be as small as possible. However, when the fund enters the market, they will be the biggest long roller, and thus levitate the roll as they execute. Beware, if you can’t predict when the fund will start to roll the majority of their positions, you will get smoked.

If you are a short roller, this is an amazing setup. As the fund spikes the roll higher, you will be able — if you are patient — to short roll at ungodly rich levels. Essentially, this ETF is a wealth transfer from the investors who hold the thing, to the short arbitrage traders supplying the bitcoin exposure.

My Precious

Many true believers exhibit elevated cortisol levels due to a fear that this ETF is akin to the ring from the Lord of the Rings — a poisoned artifact that brings one closer to the devil. They cite the belief that the rise of paper derivatives in the gold and silver markets only served to apply negative pressure to the spot markets. This is due to the ability of bullion banks to run naked shorts and balance their books using dubious accounting treatment of unallocated and allocated metal inside the LBMA warehouse.

One moment, repeat after me:

I must not fear.

Fear is the mind-killer.

Fear is the little-death that brings total obliteration.

I will face my fear.

I will permit it to pass over me and through me.

And when it has gone past, I will turn the inner eye to see its path.

Where the fear has gone there will be nothing. Only I will remain.

Ok, feeling better? This fear is evidence of a fundamental misunderstanding of the difference between bitcoin and other hard money assets.

Gold, silver, and other forms of commodity money have weight. Bitcoin is weightless. 1 BTC and 1,000,000 BTC weigh the same amount … nothing. 1 kg of gold and 1,000 kg of gold obviously weigh vastly different amounts, and require a completely different mechanism of storage. That is why large quantities of commodity money must be centrally stored. It is virtually impossible to store even moderate amounts of wealth in gold without being noticed.

Bitcoin is not owned or stored by central, commercial, or bullion banks. It exists purely as electronic data, and, as such, naked shorts in the spot market will do nothing but ensure a messy destruction of the shorts’ capital as the price rises. The vast majority of people who own commodity forms of money are central banks who it is believed would rather not have a public scorecard of their profligacy. They can distort these markets because they control the supply.

Because bitcoin grew from the grassroots, those who believe in Lord Satoshi are the largest holders outside of centralised exchanges. The path of bitcoin distribution is completely different to how all other monetary assets grew.

Derivatives, like ETFs and futures, do not alter the ownership structure of the market to such a degree that it suppresses the price. You cannot create more bitcoin by digging deeper in the ground, by the stroke of a central banker’s keyboard, or by disingenuous accounting tricks. Therefore, even if the only ETF issued was a short bitcoin futures ETF, it would not be able to assert any real downward pressure for a long period of time because the institutions guaranteeing the soundness of the ETF would not be able to procure or obscure the supply at any price thanks to the diamond hands of the faithful.